AI in P&C insurance underwriting

AI in P&C underwriting uses machine learning and automation to collect, analyze, and evaluate property and casualty insurance data. It improves underwriting speed, accuracy, and risk assessment by processing large datasets, identifying patterns, and supporting underwriters with predictive insights.

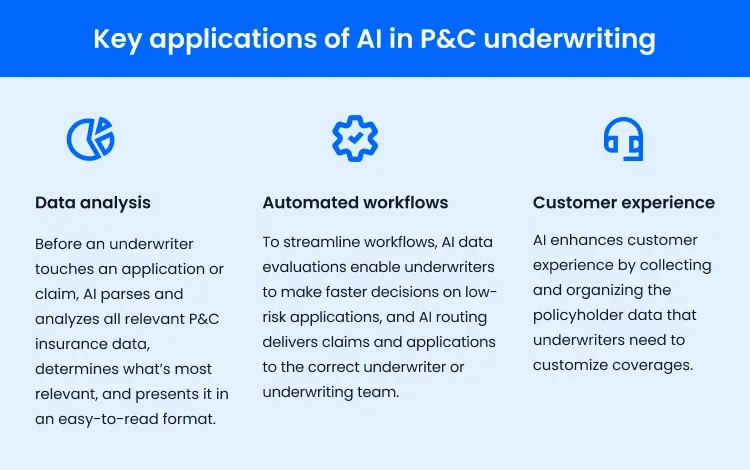

Key applications of AI in P&C underwriting

- Before an underwriter touches an application or claim, AI parses and analyzes all relevant P&C insurance data, determines what’s most relevant, and presents it in an easy-to-read format.

- To streamline workflows, AI data evaluations enable underwriters to make faster decisions on low-risk applications, and AI routing delivers claims and applications to the correct underwriter or underwriting team.

- AI enhances customer experience by collecting and organizing the policyholder data that underwriters need to customize coverages.

However, AI only delivers accurate results when it relies on valid data. When underwriters power AI with Smarty’s address data solutions, they get the reliable insights needed to do what they do best—make underwriting decisions with confidence. Give these tools a try! They’ve been tailored to fit P&C insurers just right.

In this article, we’ll talk all things AI and underwriting:

What is AI for insurance underwriting?

AI solutions for property insurance underwriting

How AI innovation is transforming property insurance underwriting

Which areas in P&C insurance will AI affect the most?

What’s ahead for AI in insurance underwriting

How can P&C insurers plan for new AI technologies?

What it takes for insurers to excel in AI

How Smarty enhances AI in P&C insurance underwriting

What is AI for insurance underwriting?

With artificial intelligence (AI) automating underwriting workflows and collecting, analyzing, and evaluating data, insurance underwriters can raise the bar (then vault over it!) by:

- Improving risk assessment for faster decisions

- Boosting customer experience with personalized policies

- Automating decisions on low-risk applications

But to do so, underwriters and AI need reliable data.

AI solutions for property insurance underwriting

Between automated decision-making and instant property risk decisions, insurance underwriting just got a whole lot faster. Here’s how AI in underwriting helps applicants, policyholders, and underwriters say goodbye to headaches and hello to victory dances.

How does AI in underwriting improve risk analysis?

When given reliable data, AI excels at processing large datasets, running quick counts to spot patterns, and then creating data summaries with predictive and actionable insights.

These capabilities reduce the time underwriters, brokers, and agents spend on data collection, recollection, rekeying, and cleanup. Before an underwriter works on an application or claim, AI can have a risk summary filled with relevant data about different forms of risk ready to rock and roll.

If your application and claim forms utilize Smarty’s US Address Autocomplete, applicants or policyholders can select verified addresses, meaning you’ll know the address AI provides in its summary is valid.

Better yet, with US Rooftop Geocoding, precise latitude and longitude coordinates for an address can be included in an AI risk summary or risk detection algorithms. Underwriters can then use a property’s geocode to quickly identify its risk zone.

Underwriters have a need for jaw-dropping speed, and with AI working in tandem with top-notch address data, that speed is within reach.

Is AI insurance underwriting improving customer experience?

By analyzing property data, AI helps underwriters customize policies to fit policyholders’ needs through underwriting prefill.

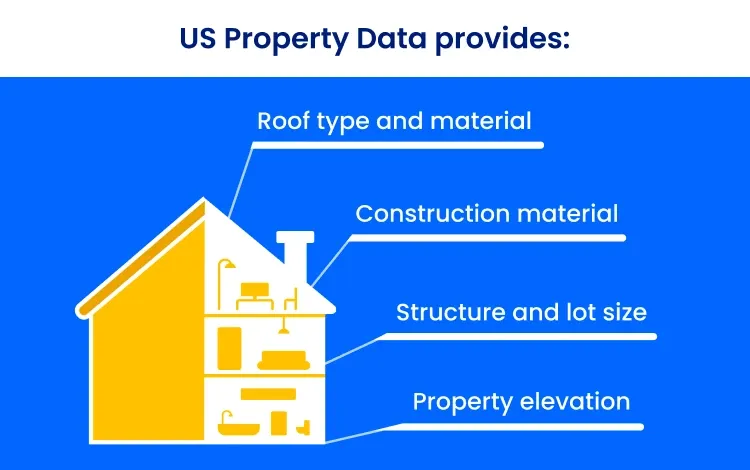

With Smarty’s US Property Data, AI can review up to 350 data points, including property characteristics, structural attributes, and financial information, then automatically answer insurance application questions.

Don’t leave insureds to guess the answers to questions like “What’s the property’s construction type?”, “What's the structure elevation?”, and “What’s the roof type?” Instead, let AI reduce the risk of bad inputs by prefilling information with up-to-date property data.

This way, both underwriters and applications save time. Underwriters avoid manual application corrections, while applicants simply verify the accuracy of the application prefill, rather than fill out the form from scratch.

With accurate, prefilled data, underwriters can better tailor policies to applicants’ needs, meaning faster, fairer underwriting and more customer satisfaction—even for customers with unusual situations.

Can AI automate decisions on low-risk applications?

With AI generating risk summaries based on real-time, accurate address data, underwriters can skip out on manual property location verification. Instead, they can make automatic decisions on low-risk applications, focus on more risky policies, and cue up their victory music.

Plus, AI can further automate underwriting decisions for low-risk applications by limiting manual investigations into insurance fraud. Working alongside fraud detection models, AI can spot fraudulent policies long before they become a problem.

Deloitte reports that by combining AI technologies with quality data, insurers can enhance their process for fraud risk detection. As AI identifies suspicious patterns in geospatial data, insurers can reduce false positives and increase the number of fraudulent policies caught by detection models. Talk about a unified fraud detection process!

While AI breezes through straightforward applications, claims, and fraudulent policies, underwriters can take their time tackling tricky, high-risk policies.

How AI innovation is transforming property insurance underwriting

AI innovations in property insurance underwriting go beyond AI’s ability to gather and evaluate data. Let’s dive into a few additional areas where AI in P&C insurance underwriting has made an impact.

AI-enhanced aerial imagery

Aerial imagery is used to remotely assess a property’s risk—think looking for roof damage or whether a backyard pool is fenced in. When integrated with risk detection algorithms, AI can automate this process by highlighting points of interest or identifying recent changes before an underwriter reviews an image.

However, even with AI enhancements and insurance automation, aerial imagery can only be as precise as the data behind it.

The best aerial imagery is high-resolution, frequently updated, and derived from multiple sources—but even these images can make it difficult to determine details like property square footage or occupancy status. To be as precise as possible, you need to eliminate guesswork by relying on clear-cut data points.

US Property Data provides insanely accurate data right at your fingertips. Roof type and material? Check. Construction material for interior and exterior walls? We won’t even break a sweat. Structure and lot size? Got it. Property elevation? All in a day’s work.

Leave imprecise aerial imagery in the rearview mirror. With real-time data, underwriters and brokers can quickly assess risk and return quotes to customers without delay.

Automated claims routing

Underwriters want to focus on what really needs their attention, not ineligible properties. Claims managers want faster and more accurate processing instead of claims managers chasing adjusters and correcting bad info.

Enter AI routing, a type of insurance automation. Before an application reaches an underwriter, AI reviews each one and then forwards it on to the right destination, meaning less wasted time and more quotes sent.

When a catastrophe occurs, AI-powered workflows speed up response times. Instead of being bottlenecked, incoming claims are quickly reviewed and routed based on their severity, allowing insurers to respond to more policyholders.

US Reverse Geocoding can further expedite disaster response times. When disasters wipe out street signs and homes, it can be challenging to assess the damage. Using reverse geocoding, alongside CAT management systems, addresses can be identified without physical markers.

Which areas in P&C insurance will AI affect the most?

You don’t have to look very far to see how AI affects P&C insurance. No, really, just scroll up.

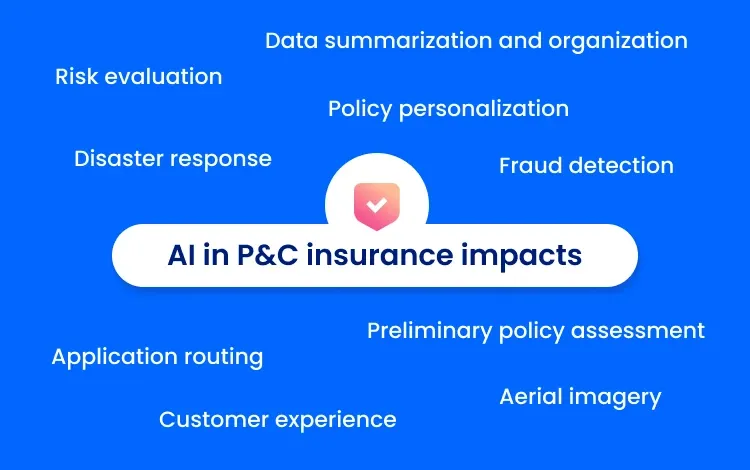

Let’s recap the highlights. AI in P&C insurance impacts:

- Risk evaluation

- Data summarization and organization

- Customer experience

- Policy personalization

- Preliminary policy assessment

- Fraud detection

- Aerial imagery

- Application routing

- Disaster response

What’s ahead for AI in insurance underwriting

The insurance digital transformation is moving faster than ever. In the 1990s, insurers moved to online platforms. By the 2010s, they’d expanded to mobile apps—leaving customers expecting cutting-edge solutions, and insurers scrambling to keep up. Now, AI has changed the rules. Again.

As AI in P&C insurance underwriting continues to play a big role in this digital glow-up, more insurers will shift to cloud-based platforms. Let’s break it down.

Migration to cloud-based solutions

If insurers want to keep up with the AI-driven digital transformation in insurance, migrating from legacy systems to modern, cloud-based ones will make integrating AI—and other property and casualty insurance software—a whole lot easier.

Unlike legacy systems, cloud-based systems are designed with integrations in mind. This means implementing an AI service won’t require a complete process overhaul. You’ll be up and running in no time.

Additionally, cloud-based solutions are designed to scale easily. Insurance underwriters now have access to more data than ever before. Your core system should be capable of scaling to handle that increase.

How can P&C insurers plan for new AI technologies?

AI technologies require modernized core systems, so for P&C insurers using legacy systems, modernizing property and casualty insurance software means AI plans can become a reality.

Modernizing core systems

At Pinpoint, Smarty’s virtual user conference, Mountain West Farm Bureau Mutual Insurance Company shared their experience migrating from a 1970s core system to Guidewire’s cloud site.

Plus, they discussed the digital transformation in insurance and how AI impacts the insurance sector at large.

Watch the session recording below to hear from the experts, or check out a full session recap!

What it takes for insurers to excel in AI

To excel in AI, P&C insurers can utilize AI’s strengths—finding patterns, quick count analytics, summarizing data, and organizing data—while investing in reliable data to steer clear of one of its weaknesses—evaluating data quality.

If you ask AI to validate an address, it won’t be able to tell you if that address actually exists. You’ll be stuck with predictions and guesswork, which isn’t quite the level of accuracy P&C insurers need.

Instead of leaving address validation up to AI, let it do what it does best. Then, plan around its strengths. You could:

- Verify your addresses, then let AI analyze them and pick out patterns, like how often your addresses include “Main Street” or ZIP Codes starting with “200.”

- Utilize AI to quickly summarize useful points of property characteristics or customers’ claims history to save countless person-hours.

- Send AI to organize your clean address data by a specific field (e.g., city, country, or numerical order).

With the right workflow integration, P&C insurers can excel in AI and underwriting.

Looking to learn more about the impact of AI on address validation? Check out our ultimate guide to AI address verification!

How Smarty enhances AI in P&C insurance underwriting

Smarty enhances AI in P&C insurance underwriting by providing the accurate data AI needs to really shine.

As we mentioned earlier, AI can’t verify an address. It can’t produce the quality data underwriters need to succeed. Smarty’s US Address Verification, on the other hand, can. With our top-of-the-line address data, you’ll be able to rest assured that the data your AI pulls from is correct.

Our address data solutions go beyond address verification. We provide:

- US Rooftop Geocoding, which turns addresses into latitude and longitude coordinates for precise risk and catastrophe modeling.

- US Reverse Geocoding to help insurers map claims following a catastrophe.

- US Property Data, a list of 350 property attributes that range from structural to financial information.

- US Address Autocomplete to streamline property applications by predicting only valid addresses.

With the data intelligence provided by these tools, P&C insurers can trust that their AI solutions produce accurate results (then break out the confetti!)

TL;DR

The machine learning and artificial intelligence hype is here to stay, and it's easy to see why. AI in P&C insurance can help underwriters analyze large property and casualty insurance datasets, automate workflows to improve underwriting speed, and enhance customer experience…at least, it can when it’s powered by the best data around.

And address data is kinda our thing. We’ll happily obsess over address verification, enrichment, autocomplete, and geocoding so you can get the most out of your AI insurance underwriting. Sign up for a free trial to see how these products integrate with your own underwriting approaches.

Learn more about address data solutions for P&C insurance.

FAQs

What is the role of AI in property and casualty (P&C) insurance underwriting?

The role of AI in P&C insurance underwriting is to analyze, summarize, and organize property and casualty insurance data. This helps underwriters save time and better customize policies.

What challenges does the P&C insurance industry face that AI can help solve?

P&C insurers need to keep up with the volume of work they receive. With AI solutions streamlining application workflows, claims processing, and data analysis, insurers can use their time and resources on what really matters and face the insurance digital transformation head-on.

How does data quality impact AI applications in insurance underwriting?

With quality address data, AI in P&C insurance underwriting can do what it does best—find patterns, quick count analytics, summarize information, and organize data with improved accuracy.

What are the key benefits of using AI in P&C insurance underwriting?

The key benefits of using AI in P&C insurance underwriting include:

- Improved data collection, analysis, and evaluation. AI quickly summarizes key data before an application or claim reaches an underwriter.

- Boosted workflow optimization. AI routes claims to the correct destination and streamlines decisions on low-risk applications.

- Better customer experiences. AI organizes customer data so underwriters can better customize policies.

Was this helpful?