Preventing identity fraud with address verification

Address verification for identity fraud prevention helps financial institutions improve address data accuracy and identity data quality by verifying that customer-provided addresses are real, valid locations. It also helps flag suspicious or invalid addresses, so financial institutions can detect fraudulent data throughout the customer lifecycle—from customer onboarding to ongoing monitoring.

Address verification supports fraud prevention throughout the customer lifecycle:

| Address verification function | Key benefit | |

| Customer onboarding | Verifying addresses during Customer Identification Program (CIP) and Know Your Customer (KYC) processes | Better customer identity verification and evaluation of fraud risk at onboarding |

| Ongoing monitoring | Continuously verifying addresses when customers update their addresses | Suspicious address changes can be flagged using up-to-date data |

With accurate address verification, financial institutions can take their identity fraud prevention workflows to the next level. To see address verification in action, check out our live demos:

Here’s what’s coming up:

Identity is breaking and the causes are structural

Why authoritative identity data matters more as fraud automates

Address data as a multi-point identity signal

Identity risk starts at data capture

Where address verification fits in a modern identity stack

Identity innovation fails faster when the basics are wrong

Identity is breaking and the causes are structural

Undetected identity fraud can create some serious challenges for financial institutions. Let’s take a closer look at two of the most common ways fraudsters can slip through the cracks.

Weak Customer Identification Programs

In the US, financial institutions are required to implement Customer Identification Programs (CIPs) as a part of their Know Your Customer (KYC) procedures. During this step of the onboarding process, financial institutions require customers to provide specific documents (like a driver’s license, business license, or trust instrument) to verify their identity.

However, customers want a quick onboarding process, and it can take time to provide the documents CIP requires to establish identity verification data.

To reduce the form friction caused by CIP procedures, finance companies in early development stages or in less-regulated markets may only require a name and email address at account creation.

While this may limit onboarding form friction, it compromises identity data quality and increases onboarding fraud risk. If fraudsters find a weak or optional CIP, they can easily fly under the radar, open multiple accounts under false identities, and launder money across platforms.

Compromised personally identifiable information

The HIPAA Journal reports that data compromises have increased 79% over the last five years, with 3,332 compromises affecting 278.8 million individuals in 2025, meaning it’s easier than ever for fraudsters to access personally identifiable information (PII).

Fake identities get a lot more convincing when they’re built on the real, deterministic identity signals provided by compromised PII. That’s why fraudsters create false identities using fabricated data AND multiple pieces of PII. This process is known as synthetic identity fraud.

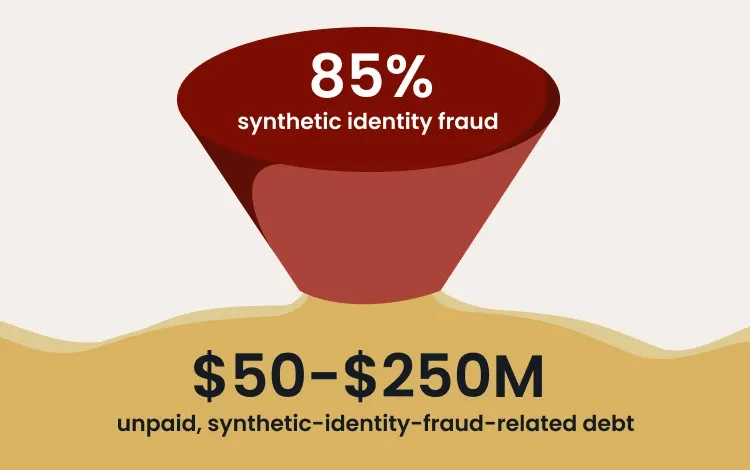

With data breaches making deterministic identity signals more accessible, synthetic identity fraud now accounts for 85% of all identity fraud cases in the US. When synthetic identity fraud slips through the cracks, US financial institutions can lose $50–$250M a year in unpaid, synthetic-identity-fraud-related debt.

Data is central to both of these identity fraud methods.

When financial institutions fail to gather the identity verification data needed to establish a reasonable belief that their customers’ identities are valid, or fail to catch indicators of synthetic identity fraud, they’re in for a world of hurt.

Why authoritative identity data matters more as fraud automates

Identity fraud prevention starts with authoritative identity data. But what happens when fraud becomes automated?

AI has enabled fraudsters to better automate fraud attempts, leaving finance companies to face several new challenges in identity fraud prevention, including:

- An inability to validate identities through visual verification alone: AI can quickly generate fake documents, so finance companies can’t exclusively rely on the visual verification of legal documents to verify a customer’s identity.

- Automated identity creation: With thousands of data breaches making PII readily available, AI can automatically compile deterministic identity signals to create false identities.

- AI-powered phishing: AI can mimic both email/texting style and voices to trick an individual into revealing PII, which can then be used as fraudulent deterministic identity signals.

To prevent automated fraud, finance companies can utilize authoritative identity data to:

- Identify inconsistencies in identity verification data: Finance companies should collect several forms of identity verification during CIP, meaning they’ll have several deterministic identity signals to compare. If something’s inconsistent, it could indicate identity fraud.

- Automate fraud prevention systems. With trusted data powering automated fraud prevention workflows, finance companies can stop automated fraud attacks in their tracks, not down the line.

- Prevent errors in manual inspections: Fraud teams can guess whether a deterministic identity signal is valid, or they can verify it against an authoritative database for greater accuracy.

Addresses are one piece of authoritative identity data, so by using address verification for identity fraud identification, finance companies can better detect and prevent fraud, whether it’s automated or not.

Let’s break down how.

Address data as a multi-point identity signal

When used as multi-point, machine-verifiable identity signals, verified addresses can go a long way.

But first, what is address verification?

To improve address data accuracy, address verification checks an address against an authoritative database to find a match. If one exists, the address is considered valid. If not, the address either doesn’t exist or isn’t registered in the database.

Beyond verifying whether an address is real, address verification in KYC, onboarding, and ongoing monitoring can also help detect signs of identity fraud.

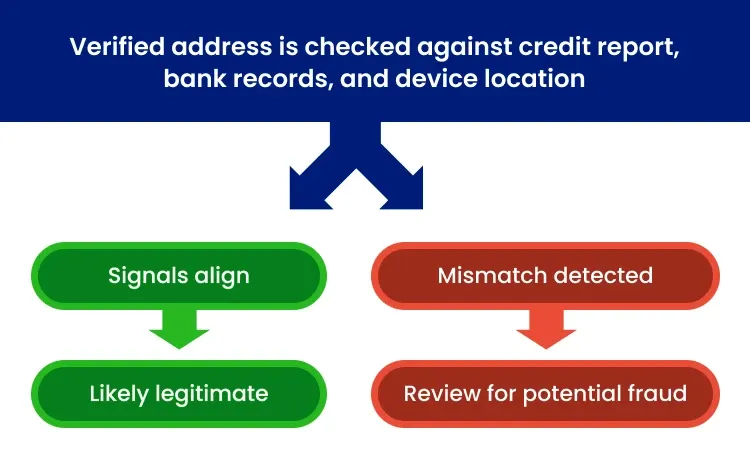

Just because an address is verified doesn’t mean it’s a customer’s actual address. To determine that, the verified address needs to be checked against the customer’s additional identity signals, such as their credit report, bank records, and device location.

If everything lines up, the address is likely legit. If something smells fishy, it may indicate identity fraud or signal that a customer or entity needs additional review.

Another way address verification can help financial institutions spot identity fraud is through address metadata.

When an address is verified, it’s often returned alongside metadata. Finance companies use these data points to flag suspicious address components that may indicate fraud risk at onboarding or during ongoing monitoring.

Here are several of the most helpful metadata points for identity fraud prevention:

DPV®

Delivery Point Validation (DPV) is the process of verifying that an entire address is present or absent from the USPS database.

An address returning as absent could mean the address doesn’t exist, but it could also mean that although the USPS won’t deliver to the address, another delivery service will. These addresses are known as non-USPS addresses.

For financial institutions, a non-USPS address isn’t necessarily a machine-verifiable identity signal or a sign of fraud. But if your address verification solution doesn’t account for the 20 million non-USPS addresses out there, you risk flagging valid addresses as invalid.

Secondary address

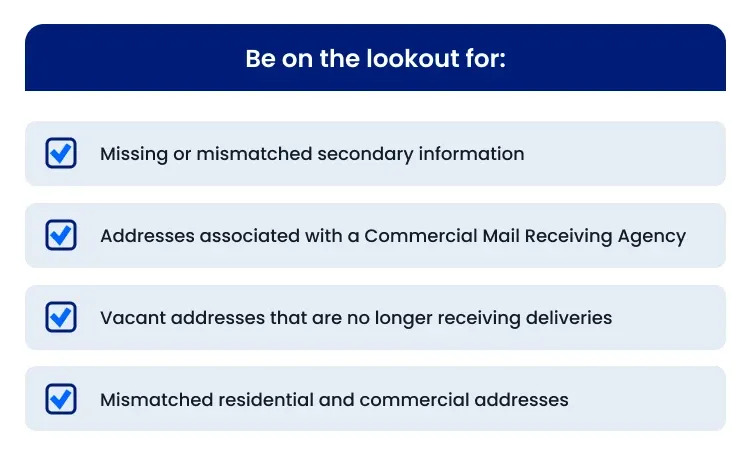

DPV can also flag issues with secondary address information by indicating whether an address exists in USPS data, but its secondary information (apartment, suite, building, etc.) either doesn’t match or is missing altogether.

Without the correct secondary information, an address isn’t fully verified. For financial institutions, this poses a threat to identity data quality and could signal fraud risk at onboarding or further along the customer lifecycle.

CMRA

A valid address could also be associated with a Commercial Mail Receiving Agency (CMRA). These are private companies, such as UPS or FedEx, that provide mailbox rental services to both individuals and companies.

If a customer provides a CMRA address during onboarding, financial institutions can’t identify the customer's location—a key aspect of CIP and KYC procedures. Plus, if an address later changes to CMRA, it could also indicate fraud.

Vacancy

Valid addresses aren’t necessarily occupied. While a delivery point may have been active in the past, it may currently be vacant and no longer receiving deliveries. When a customer uses a vacant address, financial institutions will likely want to investigate further.

RDI

A residential delivery indicator (RDI) specifies whether an address is residential or commercial. On its own, RDI isn’t a machine-verifiable identity signal or proof of fraud, but when it signals that an applicant’s story doesn’t align with their address, it can be a useful way to flag suspicious applications.

Identity risk starts at data capture

With validated addresses and metadata, finance companies can use address verification for identity fraud prevention from the moment a customer is onboarded. Plus, identifying fraud risk at onboarding with machine-verifiable identity signals helps prevent problems throughout the customer lifecycle.

Onboarding

KYC is a regulatory process that helps finance companies verify a customer’s identity and assess the risk the customer poses. As part of KYC, customers’ addresses are collected to prevent onboarding fraud risk.

Address verification in KYC procedures confirms whether customers’ addresses are real, then provides address metadata to help finance companies detect onboarding fraud risk. Otherwise, the customers’ physical locations are never checked.

Without address verification in KYC procedures, invalid addresses—whether they’re incorrect, incomplete, fabricated, or false—can corrupt your identity data quality from the start. That can lead to problems down the road.

Risk assessment

After collecting customer data during onboarding, finance companies evaluate customers’ onboarding fraud risk through a process called Customer Due Diligence (CDD). However, if the address data provided during onboarding is incorrect because a finance companies didn’t include address verification in KYC, this risk assessment might be inaccurate.

Ongoing monitoring

After onboarding and risk assessment, finance companies still need to monitor customer transactions, update their identity verification data, and report suspicious activity.

So when an invalid address gets through onboarding, it can be trusted, funded, and used before anyone catches on.

Best-case scenario, you’re contacting customers and cleaning up records once someone does catch on. Worst-case scenario, you’re triggering manual reviews and filing Suspicious Activity Reports (SARs).

Want to avoid that headache? Use address verification for identity fraud prevention in the first place.

Where address verification fits in a modern identity stack

Address verification remains an important part of an identity stack beyond onboarding. Here’s where you may find address verification crops up:

- Ongoing monitoring: Just because a customer’s identity was verified during onboarding doesn’t mean things can’t change down the road. When a customer’s address changes after onboarding, it can be re-verified to quickly detect identity fraud signals or even flag ambiguous addresses so customers can identify their actual address before a delivery or transaction is made.

- Database cleansing: Regularly standardizing your address database makes it easy to spot duplicates. If a customer’s address matches one already in your database, you’ll be able to quickly identify and investigate it.

- Successful deliveries: Many financial institutions send sensitive documents and payment cards directly to customers. Getting their addresses right helps deliveries reach the intended customer, not a fraudster.

Address validation doesn’t verify identities on its own—but it’s an essential part of preventing identity fraud. With reliable addresses alongside other machine-verifiable identity signals, your identity stack can maintain high address data accuracy and identity data quality.

Identity innovation fails faster when the basics are wrong

The tools finance companies use to prevent fraud keep evolving, but even the most advanced systems are only as good as the data behind them.

That’s why identity verification data matters. If basic data like names, email addresses, and physical addresses are wrong, the best identity fraud prevention workflows will fail.

When address verification for identity fraud maintains your address data accuracy from the start, it’s a whole lot easier to catch fraud risk at onboarding and throughout the customer lifecycle.

Plus, lightning-fast address verification can reduce the time spent on manual address fixes, audits, and SARs—and the dollars you might spend on compliance fines.

The latest identity fraud prevention solutions can put finance companies ahead of the curve, and with top-notch address data accuracy, they’re even stronger.

TL;DR

As fraud enters the age of AI and becomes increasingly sophisticated, the impact of authoritative data sources is higher than ever. As part of an exhaustive ID and anti-fraud program, address verification for identity fraud prevention helps financial institutions keep their address data clean and flag potential bad actors.

By confirming addresses against authoritative databases through address verification in KYC processes like CIP and CDD, financial institutions can:

- Identify onboarding fraud risk

- Reduce inaccurate risk assessments

- Limit manual cleanup downstream

Re-verifying address changes during ongoing monitoring also helps financial institutions:

- Detect duplicate addresses

- Send payment cards to the right customer

- Identify suspicious address changes over time

If your identity data quality could use a glow-up, try our US and International Address Verification tools free for 42-days—and get the address data accuracy you’ve been missing.

Was this helpful?